It isn’t just GameStop:

Here are some of the other heavily shorted stocks shooting higher

Suffering theater chain, fallen cellphone giant and another damaged retailer are among shorted stocks finding big gains on Wall Street

The dynamic that has seemingly contributed to a short squeeze in the stock of videogame retailer GameStop Corp. also appears to be affecting shares in a host of other heavily shorted companies.

Referenced Symbols

AMC +12.22% BB +4.94% EXPR -26.75% GME +92.71% FB +1.45% BBBY +20.18% KOSS +66.67%

The dynamic that has seemingly contributed to a short squeeze in the stock of videogame retailer GameStop Corp. also appears to be affecting shares in a host of other heavily shorted companies.

AMC Entertainment Holdings Inc. AMC, +12.22%, BlackBerry Ltd. BB, +4.94% and retailer Express Inc. EXPR, -26.75%, have all experienced sharp moves without any apparent news to act as a driver while facing a large amount of bets against them. The same dynamic exists for GameStop GME, +92.71% stock, which has gained more than 300% in the past two-plus weeks amid support from investors on Reddit’s WallStreetBets message board.

In the case of AMC, the world’s biggest cinema operator, that has meant gains of more than 120% in the year to date, even as the company has conducted dilutive capital raisings and its core business.

‘Investor stampede’ squeezes out bears

Shares of struggling retailer Express were among those caught up in the apparent short squeeze, according to Wedbush analyst Jen Redding, as the stock more than tripled (up 255%) in two days on record volume despite no news released by the company.

The stock skyrocketed 132% on Monday on volume of 358.6 million shares on Monday, both one-day records, breaking the previous records set on Friday with a 53% gain on volume of 77.3 million shares. In comparison, the full-day average volume over the past 30 days has been 18.9 million shares.

The company confirmed to MarketWatch that it’s last public announcement was made on Jan. 14, when the stock shot up 24% on volume of about 51 million shares after Express revealed an agreement on $140 million in additional financing with Sycamore Partners, as well as Wells Fargo and Bank of America. This financing was definitely good news for a retailer that has been fighting to stay solvent. But the stock fell 9.4% over the next three days, so it’s unlikely the Friday-Monday rally was a result of that news.

“We’re focused on our EXPRESSway Forward transformation strategy and things that are in our control,” said Dan Aldridge III, vice president of investor relations, in an emailed statement.

In addition to the “wider squeeze play” of the more shorted stocks, Wedbush’s Redding said the stock benefited from an “investor stampede” following bullish comments from a Twitter “personality” Will Meade.

Meade’s Twitter profile says he’s a former portfolio manager at a Goldman Sachs founded $1 billion hedge fund, with over 127,000 followers (he’s not verified).

On Jan. 22, just before Express’s two-day rocket ride, Meade tweeted that Express’s stock fit the criteria of being the next GameStop, as it had a low stock price, had a retail brand name that could turn around and had high short interest levels, at about 13% of the public float.

Globe says Bouvier keeps Whitecap at "sector perform"

2021-01-21 08:36 ET - In the News

The Globe and Mail reports in its Thursday edition that Scotia Capital analyst Jason Bouvier hiked his target for Whitecap Resources ($5.27) to $6 from $2.50 with a "sector perform" rating after coming off research restrictions. The Globe's David Leeder writes in the Eye On Equities column that analysts on average target the shares at $5.43. Mr. Bouvier says in a note: "We believe the cumulative $1.1-billion in transactions provide Whitecap with the critical mass and operational overlap necessary to lower its cost structure. In addition, we believe the increased scale will help attract institutional investor interest." The Globe reported on Feb. 1 and July 1 that Desjardins Securities analyst Scott Van Bolhuis was keeping his rating at "buy." The shares could then be had for $4.82 and $2.23. The Globe reported on Aug. 24 that Desjardins Securities analyst Chris MacCulloch assumed coverage on Whitecap Resources with a "buy" rating and $3.75 share target. The shares could then be had for $2.43. The Globe reported on Dec. 10 that Raymond James analyst Jeremy McCrea had upgraded Whitecap to "strong buy" from "outperform," while bumping his share target up by $1.25 to $5.50. The shares were then worth $4.52.

© 2021 Canjex Publishing Ltd. All rights reserved.

Whitecap Resources to pay 0.0142-cent dividend Feb. 15

2021-01-14 17:11 ET - News Release

An anonymous director reports

WHITECAP RESOURCES INC. CONFIRMS MONTHLY DIVIDEND FOR JANUARY OF $0.01425 PER SHARE

Whitecap Resources Inc. will pay a cash dividend of .01425 cents per common share in respect of January operations on Feb. 15, 2021, to shareholders of record on Jan. 31, 2021. This dividend is an eligible dividend for the purposes of the Income Tax Act (Canada).

About Whitecap Resources Inc.

Whitecap Resources is an oil-weighted growth company that pays a monthly cash dividend to its shareholders. Its business is focused on profitable production growth combined with sustainable dividends to shareholders. The company's objective is to fully finance its capital expenditures and dividend payments within funds flow.

© 2021 Canjex Publishing Ltd. All rights reserved.

The Canadian oil and gas industry had already faced years of headwinds leading into 2020.

This included stalled or cancelled infrastructure projects resulting in Western Canadian producers receiving discounted pricing as U.S. shale production soared; carbon taxes and new regulations designed to accelerate the transition to green energy, which increased regulatory uncertainty and operating costs; and declining investment and capital spend in the sector, with accompanying job losses, since 2014.

Then came the challenges of 2020. Early in the year, Saudi Arabia and Russia commenced a price war that resulted in plummeting commodity prices just as the world's response to the COVID-19 pandemic instantly eliminated almost 30 million barrels per day of global oil demand. This created an over-supplied market that ultimately saw commodity prices sink to unprecedented negative numbers in the spring.

In the wake of unprecedented challenges, green shoots of M&A activity are beginning to appear as the industry repositions itself for recovery.

Commodity prices improved over the summer and fall as energy demand recalibrated with the gradual reopening of the world economy. Oil demand ultimately closed the year only 10% lower than pre-COVID-19 levels. While the outlook improved with the announcement of multiple successful COVID-19 vaccines and OPEC+'s new deal on production, the COVID-19 crisis is far from over and many other challenges remain. Companies continue to adjust to carbon taxes and new regulations, including the impact of the proposed new Clean Fuel Standard regulations expected to come into effect in 2022, and the Canadian government's recently announced climate plan that will see the carbon tax surge, from $50 per tonne in 2022 to $170 per tonne by 2030.

Lack of pipeline capacity also remains an issue, although there is now a clear pathway to completion of two of the three main crude export pipeline projects (the Trans Mountain expansion and Enbridge's Line 3 replacement), while Keystone XL remains in jeopardy with the new Biden administration in Washington. In addition, the $40 billion LNG Canada project is now almost two years into construction, with hopes of opening by 2025. These major projects involve significant capital spend and job creation and are an important catalyst for economic recovery in the post-COVID-19 era.

Substantial uncertainty continues to prevail in the Canadian oil and gas industry. Despite positive signals in commodity and share prices, near-term energy demand recovery remains tenuous as COVID-19 case numbers and lockdowns worsen, and the timing and outcome of the vaccine rollout remain unclear. Meanwhile, the green energy movement continues to build momentum, while investor support and capital for fossil fuels are increasingly constrained.

Although M&A activity was muted for most of 2020, green shoots are beginning to appear as a combination of factors begin to drive deal activity. We expect to see a combination of the following trends over the course of the next year.

After a litany of country exits by foreign companies over the last several years, the Canadian oil and gas industry has seen a flurry of consolidation activity, headlined by the Cenovus-Husky all-stock merger valued at $23.6 billion (on an enterprise basis for both companies). Other transactions include CNRL's acquisition of Painted Pony, Whitecap's acquisitions of TORC and NAL Resources and Tourmaline's acquisitions of Modern Resources and Jupiter Resources. We expect this trend to continue as companies look to combine their operations in order to achieve scale and cost and capital synergies and, in some cases, rebalance the weighting of their asset portfolios toward natural gas. Deal activity is also expected to be driven by companies with liquidity issues, as they seek out mergers to strengthen balance sheets or complete restructurings of their debt. Certain leveraged companies that have been struggling to weather the storm may reach the tipping point with boards and lenders determining that insolvency proceedings are unavoidable in light of continued distress in the industry and a longer timeline for recovery. These distressed sales may provide buyers the opportunity to acquire assets at a discount.

It is noteworthy that recent M&A activity has been driven by domestic strategic acquirors, with foreign and institutional investors mostly remaining on the sidelines for now. However, as investor appetite for U.S. shale wanes, the world-class Montney natural gas play could be a bright spot for Canada. It remains to be seen whether ConocoPhillips's acquisition of additional Montney acreage from Kelt Exploration in July is a harbinger of a gradual return of foreign investment to Western Canada.

Any large-scale consolidation is likely to result in an increase in non-core asset sales as these new merged entities seek to focus on their core business. Additionally, large companies are expected to divest end-of-life assets and other non-core assets as they clean up their balance sheets. This presents an opportunity for well-funded junior and mid-size companies to acquire high-quality assets and implement optimization strategies, as well as for management teams with successful track records to partner with financial investors on new investment platforms. While interest from private equity sponsors in midstream infrastructure has remained robust over the last several years, it remains to be seen whether pricing and cash generation are sufficiently attractive for them to pursue opportunistic investments in the upstream space.

In light of the current state of economic instability and ongoing uncertainty in the energy demand and oil price outlook, there is likely to be dislocation in valuation expectations between sellers and buyers. Stock deals are common in the current environment, as sellers are able to participate in future recovery and upside, while buyers are able to preserve cash and avoid additional leverage on their balance sheets. Market volatility has also resulted in increased interest in earn-outs, contingent payments and other similar structures to bridge value gaps, allocate risk and give parties the confidence to transact if they are able to share in the upside of recovery. These structures are often time-consuming to negotiate and, not infrequently, give rise to post-closing disputes. Nevertheless, greater interest in these structures is likely to continue in the current volatile environment.

Despite the dominant media narrative implying an imminent transition to green energy, this polarizing view does not fit reality. The consensus among leading industry analysts and participants is that the long-term growth in global energy demand will require a combination of conventional and renewable energy sources for decades to come. Fossil fuels will remain an important component in the energy mix and will contribute to the economic recovery of our resource-rich country as the energy transition unfolds over time. For example, while the costs of solar and wind have declined, natural gas is still required to resolve intermittency issues (as the scaling and technology of battery storage are still in their infancy). Meanwhile, on a global scale, the completion of the Trans Mountain expansion and LNG Canada projects represent an opportunity for Canadian oil and gas to replace coal-burning plants in Asia.

Despite the dominant media narrative implying an imminent transition to green energy, this polarizing view does not fit reality.

Canadian oil and gas companies have made great strides on the ESG front and continue to demonstrate their commitment to operating to the highest environmental and social standards. A number of larger Canadian oil and gas companies have recently committed to a net-zero emissions target and are developing strategies to achieve that goal. Canadian oil and gas companies are already global leaders in R&D investment on a per barrel basis, which has resulted in significant reductions in emissions, water use and land footprint over the last decade. The industry is uniquely situated to develop a number of capital-intensive clean energy technologies such as carbon capture, storage and utilization, hydrogen, biofuels, offshore wind and battery storage—and we expect industry to provide significant support, funding and deal activity in the clean energy sector. The Canadian and Albertan governments have recently launched a number of complementary investment programs to support these initiatives, and we expect financial investors will also continue to have a strong appetite to partner in energy transition projects. Companies and assets with strong ESG performance will have a strategic edge in attracting capital and gaining stakeholder support for future transactions and projects.

The Canadian oil and gas industry will be a key contributor to the near-term economic recovery of the country in the post-COVID-19 era. It is also positioned to be a leader in achieving a lower-carbon future over time. The sector is hoping to find public support on both fronts—as the responsible energy supplier of choice (with a leading environmental track record and standards), and a ready contributor to the Canadian economy through jobs, capital investment and government revenue.

| House Positions for C:MDNA from 20210120 to 20210120 |

| House | Bought | $Val | Ave | Sold | $Val | Ave | Net | $Net |

|---|---|---|---|---|---|---|---|---|

| 79 CIBC | 55,631 | 306,455 | 5.509 | 18,500 | 101,499 | 5.486 | 37,131 | -204,956 |

| 5 Penson | 4,435 | 23,800 | 5.366 | 2,600 | 14,147 | 5.441 | 1,835 | -9,653 |

| 80 National Bank | 2,501 | 13,492 | 5.395 | 1,880 | 10,285 | 5.471 | 621 | -3,207 |

| 72 Credit Suisse | 400 | 2,214 | 5.535 | 0 | 400 | -2,214 | ||

| 13 Instinet | 300 | 1,680 | 5.60 | 0 | 300 | -1,680 | ||

| 85 Scotia | 236 | 1,244 | 5.271 | 0 | 236 | -1,244 | ||

| 74 GMP | 2,000 | 10,500 | 5.25 | 1,800 | 9,990 | 5.55 | 200 | -510 |

| 39 Merrill Lynch | 900 | 4,866 | 5.407 | 700 | 3,915 | 5.593 | 200 | -951 |

| 212 Virtu | 155 | 827 | 5.335 | 0 | 155 | -827 | ||

| 14 ITG | 0 | 179 | 931 | 5.201 | -179 | 931 | ||

| 53 Morgan Stanley | 480 | 2,551 | 5.315 | 1,200 | 6,802 | 5.668 | -720 | 4,251 |

| 91 Jones | 0 | 1,000 | 5,558 | 5.558 | -1,000 | 5,558 | ||

| 33 Canaccord | 0 | 1,200 | 6,720 | 5.60 | -1,200 | 6,720 | ||

| 2 RBC | 223 | 1,266 | 5.677 | 3,246 | 17,456 | 5.378 | -3,023 | 16,190 |

| 1 Anonymous | 15,306 | 83,820 | 5.476 | 22,320 | 122,263 | 5.478 | -7,014 | 38,443 |

| 89 Raymond James | 0 | 9,900 | 53,460 | 5.40 | -9,900 | 53,460 | ||

| 7 TD Sec | 11,390 | 60,830 | 5.341 | 29,432 | 160,518 | 5.454 | -18,042 | 99,688 |

| TOTAL | 93,957 | 513,545 | 5.466 | 93,957 | 513,544 | 5.466 | 0 | -1 |

News

In company news, Moderna (MRNA) publishing late-stage data confirming the efficacy and safety of its mRNA-1273 vaccine candidate, with the messenger RNA-based vaccine preventing COVID-19 in 94.1% of the trial participants receiving the two-dose regimen 28 days apart. Of the nearly 30,000 volunteers participating in the study, only 11 of the 196 cases of COVID-19 were in the active group, according to the trial results published in the New England Journal of Medicine. US regulators approved emergency use of mRNA-1273 earlier this month.

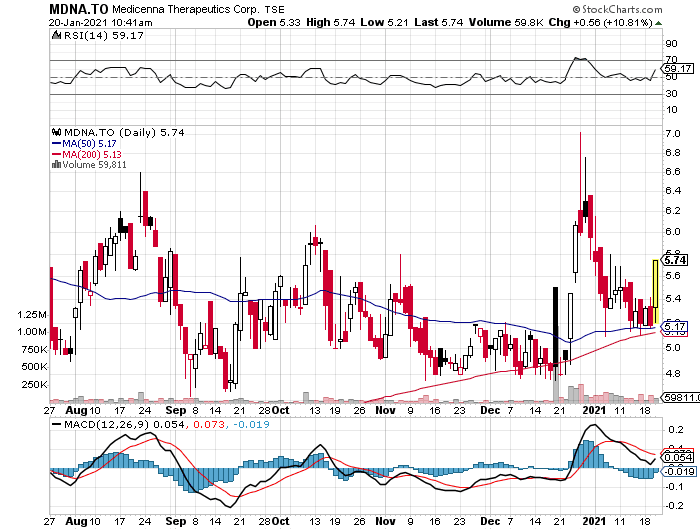

Medicenna Therapeutics (MDNA) the Canadian immuno-oncology firm announced an at-the-market offering of up to $25 million of its common shares from time to time. Net proceeds will be used for general corporate purposes, including working capital, research and development, and clinical trial costs, the company said.

On January 6, 2021, Fahar Merchant, President and Chief Executive Officer of Medicenna Therapeutics Corp. ("Medicenna"), purchased an aggregate of 10,000 common shares of Medicenna (the "Shares") through the facilities of the Toronto Stock Exchange at prices ranging from $5.13 to $5.18, for an aggregate consideration of $51,778 (the "Transaction").

Prior to the Transaction, (i) Dr. Merchant beneficially owned an aggregate of 5,250,000 Shares, options ("Option") to purchase an aggregate of 1,377,299 Shares and 100,000 common share purchase warrants exercisable at a price of $1.20 per Share until December 21, 2023 (the "Warrants"); (ii) Ms. Rosemina Merchant, a joint actor with Dr. Merchant, beneficially owned 5,250,000 Shares, Options to purchase 834,637 Shares and 100,000 Warrants; and (iii) Aries Biologics Inc. ("Aries") an entity jointly-owned by Dr. Merchant and Ms. Merchant, beneficially owned an aggregate of 5,500,000 Shares. Together, Dr. Merchant and Ms. Merchant beneficially owned, directly and through Aries, an aggregate of 16,000,000 Shares, 2,211,936 Options and 200,000 Warrants, representing 31.68% of the currently issued and outstanding Shares on a non-diluted basis, and 34.79% of the currently issued and outstanding Shares on a partially-diluted basis, assuming exercise of the Options and Warrants held by Dr. Merchant and Ms. Merchant only.

Following the Transaction, (i) Dr. Merchant beneficially owns an aggregate of 5,260,000 Shares, Options to purchase an aggregate of 1,377,299 Shares and 100,000 Warrants; (ii) Ms. Rosemina Merchant beneficially owns 5,250,000 Shares, Options to purchase 834,637 Shares and 100,000 Warrants; and (iii) Aries beneficially owns an aggregate of 5,500,000 Shares. Together, Dr. Merchant and Ms. Merchant beneficially own, directly and through Aries, an aggregate of 16,010,000 Shares, 2,211,936 Options and 200,000 Warrants, representing 31.70% of the currently issued and outstanding Shares on a non-diluted basis, and 34.81% of the currently issued and outstanding Shares on a partially-diluted basis, assuming exercise of the Options and Warrants held by Dr. Merchant and Ms. Merchant only.

Dr. Merchant and Ms. Merchant, as Medicenna's President and Chief Executive Officer and Chief Development Officer, respectively, in addition to together being Medicenna's largest shareholders, have been and will continue to be actively involved in the business, operations and strategic planning for Medicenna. The Shares beneficially owned by Dr. Merchant and Ms. Merchant, directly and through Aries, are held for investment purposes. Each of them intends to review on a continuing basis his or her investment in Medicenna and may, depending on market and other conditions, increase or decrease his or her beneficial ownership of securities of Medicenna through market transactions, private agreements, public offerings or otherwise.

Dr. Merchant relied on the normal course purchase exemption from the take-over bid rules contained in Section 4.1 of National Instrument 62-104 - Take-Over Bids and Issuer Bids with regards to the Transaction.

An early warning report relating to this transaction will be filed on SEDAR under Medicenna's profile at www.sedar.com. To obtain a copy of such report, please contact Ms. Elizabeth Williams, Chief Financial Officer of Medicenna at 416-648-5555. Medicenna's head office is located at 2 Bloor Street W., 7(th) Floor, Toronto, ON, M4W 3E2. Dr. Merchant's mailing address is 2 Bloor Street W., 7(th) Floor, Toronto, ON, M4W 3E2.

SOURCE Fahar Merchant

View original content: http://www.newswire.ca/en/releases/archive/January2021/07/c5430.html

SOURCE: Fahar Merchant

News

2020-12-30 18:20 ET - News Release

Ms. Elizabeth Williams reports

MEDICENNA ESTABLISHES AT-THE-MARKET SALES FACILITY

Medicenna Therapeutics Corp. has entered into a sales agreement with SVB Leerink acting as sales agent, pursuant to which the company may, from time to time sell, through "at-the-market" offerings on the Nasdaq Capital Market such number of common shares as would have an aggregate offering price of up to $25-million (U.S.) under the ATM prospectus supplement (as defined below).

SVB Leerink, at Medicenna's discretion and instruction, will use its commercially reasonable efforts to sell the common shares at prevailing market prices from time to time. No offers or sales of common shares will be made in Canada or through the facilities of the Toronto Stock Exchange. The ATM offering will be made by way of a prospectus supplement to the company's Canadian final base shelf prospectus, as amended, and the company's United States final base shelf prospectus, which is contained in the company's U.S. registration statement on Form F-10 (file No. 333-238905), dated July 28, 2020, and declared effective by the United States Securities and Exchange Commission on July 30, 2020.

The ATM prospectus supplement has been filed in Canada with the Ontario Securities Commission, as principal regulator, the British Columbia Securities Commission and the Alberta Securities Commission, and in the United States with the SEC. The TSX has conditionally approved the ATM offering and the Nasdaq has been notified of the ATM offering.

The company plans to use the net proceeds of the ATM offering, if any, for general corporate purposes including, but not limited, to working capital expenditures, research and development expenditures, and clinical trial expenditures.

The ATM offering will terminate upon the earlier of (a) the sale of $25-million (U.S.) of common shares subject to the sales agreement, (b) the termination of the sales agreement by SVB Leerink or the company, as permitted therein, or (c) Aug. 28, 2022.

Copies of the ATM prospectus supplement will be available upon request by contacting SVB Leerink LLC, attention: Syndicate Department, One Federal St., 37th floor, Boston, Mass., 02110, by telephone at 1-800-808-7525, extension 6132, or by e-mail at syndicate@sbvleerink.com. The ATM prospectus supplement (together with the related base shelf prospectus) is also available on the SEC's website. Before you invest, you should read the ATM prospectus supplement and the related base shelf prospectus and other documents that the company has filed with the SEC for more complete information about the company, the sales agreement and the ATM offering.

About Medicenna Therapeutics Corp.

Medicenna is a clinical-stage immunotherapy company focused on the development of novel, highly selective versions of IL-2, IL-4 and IL-13 superkines, and first-in-class empowered cytokines (ECs) for the treatment of a broad range of cancers. Medicenna's long-acting IL2 superkine asset, MDNA11, is a next-generation IL-2 with superior CD122 binding without CD25 affinity, and therefore preferentially stimulating cancer-killing effector T cells and NK cells when compared with competing IL-2 programs. It is anticipated that MDNA11 will be ready for the clinic in 2021. Medicenna's lead IL4-EC, MDNA55, has completed a phase 2b clinical trial for rGBM, the most common and uniformly fatal form of brain cancer. MDNA55 has been studied in five clinical trials involving 132 subjects, including 112 adults with rGBM. MDNA55 has obtained fast track and orphan drug status from the FDA and FDA/EMA (European Medicines Agency), respectively.

We seek Safe Harbor.

© 2021 Canjex Publishing Ltd. All rights reserved.

TORONTO, ON / ACCESSWIRE / January 18, 2021 / 01 Communique Laboratory Inc. (TSXV:ONE)(OTCQB:OONEF) (the “Company”) one of the first-to-market, enterprise level cybersecurity providers for the quantum computing era, today announced a Bounty Contest. You are invited to join the Bounty Contest 2021 (February 22 - March 22) for the chance to win a grand prize of CAD100,000 in cash. This Bounty Contest is exclusively sponsored by PwC China.

As the race for quantum supremacy intensifies, so is the concern over cyber security. Quantum computers could very well crack traditional encryption earlier than we expect. Canadian Company 01 Communique claims that its cryptography technology, IronCAP™ can be deployed on existing computers in order to protect them against the quantum threat. It is prepared to put IronCAP™ to the test in the Bounty Contest.

Andrew Cheung enthusiastically stated, “This Bounty Contest is an ideal platform for participants who are innovators, researchers, scientists, domain experts, academics to test our IronCAP™ technology. I am confident that IronCAP™ can face these challenges and ultimately earn recognition as the best-in-class quantum safe solution. Having PwC China’s support in this important exercise is of particular significance given China’s advanced research and development capability in Quantum technology.”

Samuel Sinn, Partner, Cybersecurity & Privacy Services, PwC China stated: “We are delighted to sponsor this Bounty Contest organized by 01 Communique Laboratory Inc. We rely on encryption technology to protect our information asset, and as we approach the Quantum age, we need a new generation of cryptographic solutions to continue to safeguard the trust we need in the digital world. This contest is an excellent opportunity for IronCAP™ to demonstrate its robustness against the quantum threat.”

Details:

The Company expects participants from around the world to test its quantum-safe encryption. Beginning on Monday, February 22 at 12am EST, participants will be given 30 days to explore IronCAP™ encryption. A cash prize of CAD100,000 will be awarded to the first person that is able to break the encryption. The result will be announced on Monday, March 22 where the outcome of the Bounty Contest will be revealed!

You can register for the event beginning February 8th online at https://ironcap.ca/ironcap-bountycontest.

About IronCAP™ and IronCAP X™:

IronCAP™ is at the forefront of the cyber security market and is designed to protect our customers from cyber-attacks. IronCAP’s patent-pending cryptographic system is designed to protect users and enterprises against the ever-evolving illegitimate and malicious means of gaining access to their data today as well as in the future with the introduction of powerful quantum computers. Based on improved Goppa code-based encryption it is designed to be faster and more secure than current standards. It operates on conventional computer systems, so users are protected today while being secure enough to safeguard against future attacks from the world of quantum computers. An IronCAP™ API is available which allows vendors of a wide variety of vertical applications to easily transform their products to ensure their customers are safe from cyber-attacks today and from quantum computers in the future.

IronCAP X™, a cybersecurity product for email/file encryption, incorporating our patent-pending technology for commercial. The new product has two major differentiations from what is in the market today. Firstly, many offerings in today’s market store users secured emails on email-servers for recipients to read, making email-servers a central target of cyber-attack. IronCAP X™, on the other hand, delivers each encrypted message end-to-end to the recipients such that only the intended recipients can decrypt and read the message. Consumers’ individual messages are protected, eliminating the hackers’ incentive to attack email servers of email providers. Secondly, powered by our patent-pending IronCAP™ technology, we believe IronCAP X™ is the world’s first quantum-safe end-to-end email encryption system; secured against cyberattacks from today’s systems and from quantum computers in the future. Consumers and businesses using IronCAP X™ will be protected by tomorrow’s cybersecurity today.

About 01 Communique

Established in 1992, 01 Communique (TSX-V: ONE; OTCQB: OONEF) has always been at the forefront of technology. The Company’s cyber security business unit focuses on post-quantum cybersecurity with the development of its IronCAP™ technology. IronCAP’s patent-pending cryptographic system is an advanced Goppa code-based post-quantum cryptographic technology that can be implemented on classical computer systems as we know them today while at the same time can also safeguard against attacks in the future post-quantum world of computing.

The Company’s remote access business unit provides its customers with a suite of secure remote access services and products under its I’m InTouch and I’m OnCall product offerings.

The remote access offerings are protected in the U.S.A. by its patents #6,928,479 / #6,938,076 / #8,234,701; in Canada by its patents #2,309,398 / #2,524,039 and in Japan by its patent #4,875,094. For more information, visit the Company’s web site at www.ironcap.ca and www.01com.com.

Cautionary Note Regarding Forward-looking Statements

Certain statements in this news release may constitute “forward-looking” statements which involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. When used in this news release, such statements use such words as “may”, “will”, “expect”, “believe”, “anticipate”, “plan”, “intend”, “are confident” and other similar terminology. Such statements include statements regarding the business prospects of IronCAP™ and IronCAP X™, the future of quantum computers and their impact on the Company’s product offering, the functionality of the Company’s products and the intended product lines for the Company’s technology. These statements reflect current expectations regarding future events and operating performance and speak only as of the date of this news release. Forward-looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the matters discussed in the forward-looking statements, including, but not limited to, a delay in the anticipated adoption of quantum computers and a corresponding delay in Q day, the ability for the Company to generate sales, and gain adoption of, IronCAP™ and IronCAP X™, the ability of the Company to raise financing to pursue its business plan, competing products that provide a superior product, competitors with greater resources and the factors discussed under “Risk and Uncertainties” in the company’s Management`s Discussion and Analysis document filed on SEDAR. Although the forward-looking statements contained in this news release are based upon what management of the Company believes are reasonable assumptions, the company cannot assure investors that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this news release, and the company assumes no obligation to update or revise them to reflect new events or circumstances.

Neither TSX Venture Exchange (“TSX-V”) nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

INVESTOR CONTACT:

Brian Stringer

Chief Financial Officer

01 Communique

(905) 795-2888 x204

SOURCE: 01 Communique Laboratory, Inc.